Confused about solar panel insurance? A solar EPC consultant explains what your homeowners policy covers, what it misses, and how to protect every component

Every large EPC solar project I consult on hits the same point in the client conversation — usually after the system design is finalised and before the installation contract is signed. The client asks: “Does my home insurance cover my solar panels?” Sometimes the answer is yes, partially. Sometimes the policy has a gap that could cost the homeowner tens of thousands of dollars after a hail storm or a falling tree. The question is always the right one. It is rarely asked early enough.

This guide gives US homeowners the same breakdown I walk EPC clients through: what a standard homeowners insurance policy covers for solar panels, what the common gaps are, which solar components are and are not covered, and what additional coverage to ask for.

| Disclaimer: This article is written by a Solar EPC Consultant based on real client inquiries and project experience. It is educational only. For your specific insurance decisions, consult a licensed insurance advisor in your state. |

1. How Homeowners Insurance Covers Solar Panels — The Baseline

In most cases, solar panels installed on a residential rooftop are covered under a standard homeowners insurance policy as part of the dwelling structure (Coverage A). The panels are treated as a permanent fixture of the home — which, once installed, they are. The standard US homeowners policy form is the HO-3 (Special Form). Under HO-3, Coverage A covers the dwelling against open perils — all causes of loss are covered except those specifically excluded. For most solar installations, this means panels are covered for: fire, lightning, windstorm, hail, theft, vandalism, falling objects, and the weight of ice or snow.

| Solar Component | Covered Under Standard HO-3? | Coverage Type | Notes |

| Solar panels (rooftop mounted) | Yes — typically | Coverage A (Dwelling) | Treated as permanent fixture of the home |

| Solar inverter (string / micro) | Yes — typically | Coverage A (Dwelling) | Mounted to structure; covered as dwelling component |

| Battery storage (e.g. Tesla Powerwall) | Yes if hardwired to structure | Coverage A or Coverage B | Portable/detached units may fall under Coverage C |

| Racking & mounting hardware | Yes — typically | Coverage A (Dwelling) | Structural attachment — covered with panels |

| DC/AC wiring & conduit | Yes — typically | Coverage A (Dwelling) | Permanent electrical installation |

| Solar monitoring system | Possibly — verify | Coverage C (Personal Property) | Smart devices may need scheduled endorsement |

| Ground-mounted solar array | Yes — Coverage B | Coverage B (Other Structures) | Typically 10% of Coverage A limit — verify limit is sufficient |

| Portable solar panels / generators | Coverage C only | Coverage C (Personal Property) | Subject to personal property limits and sub-limits |

| EV charger powered by solar | Possibly — verify | Coverage A or B | Depends on attachment to structure; confirm with insurer |

| Engineer’s Note: On a 120 kW commercial rooftop project in Texas, the building owner assumed the solar array was automatically covered under the existing commercial property policy. It was not — the insurer required a scheduled equipment floater for the inverters and battery bank as they exceeded the policy’s standard equipment sub-limit. Always confirm coverage in writing before energisation, not after a loss event. |

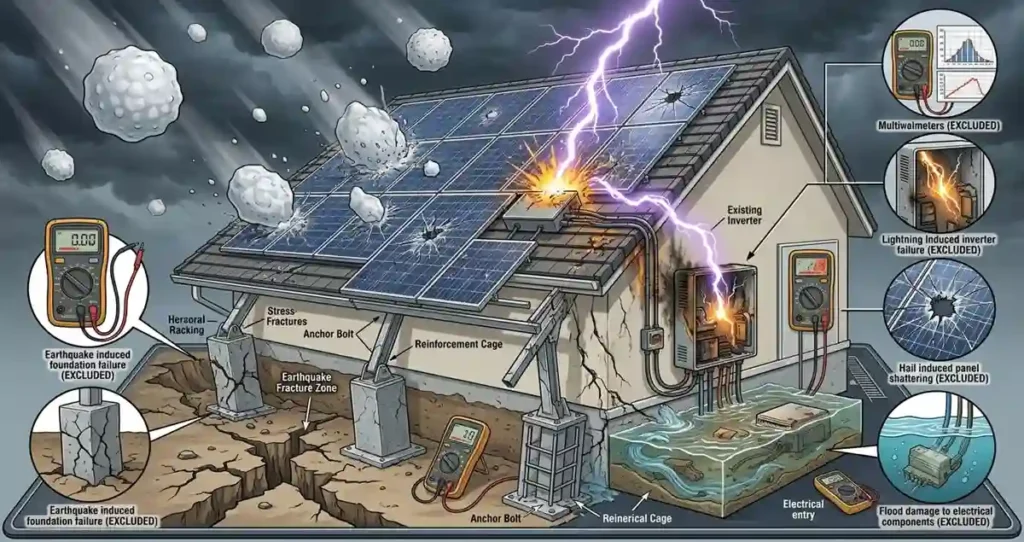

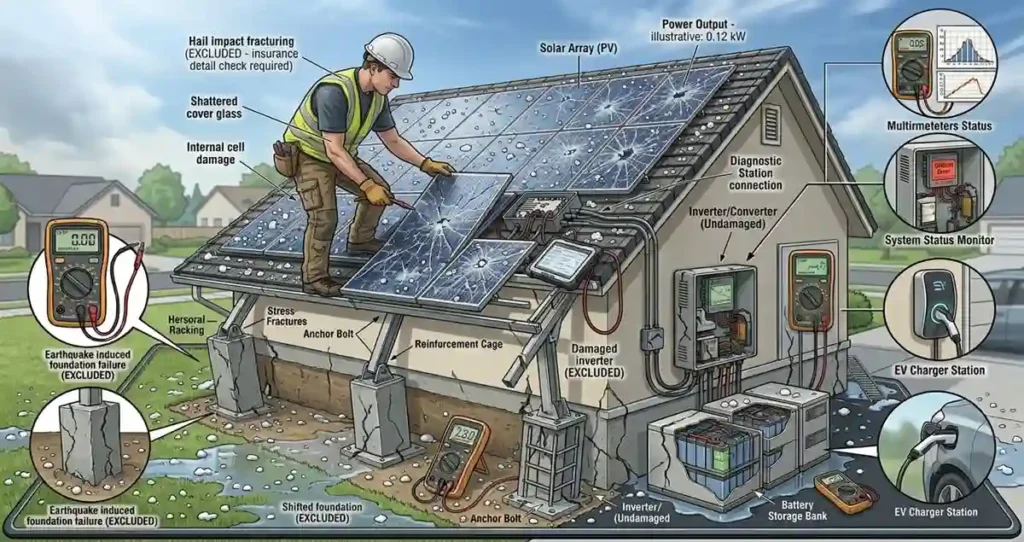

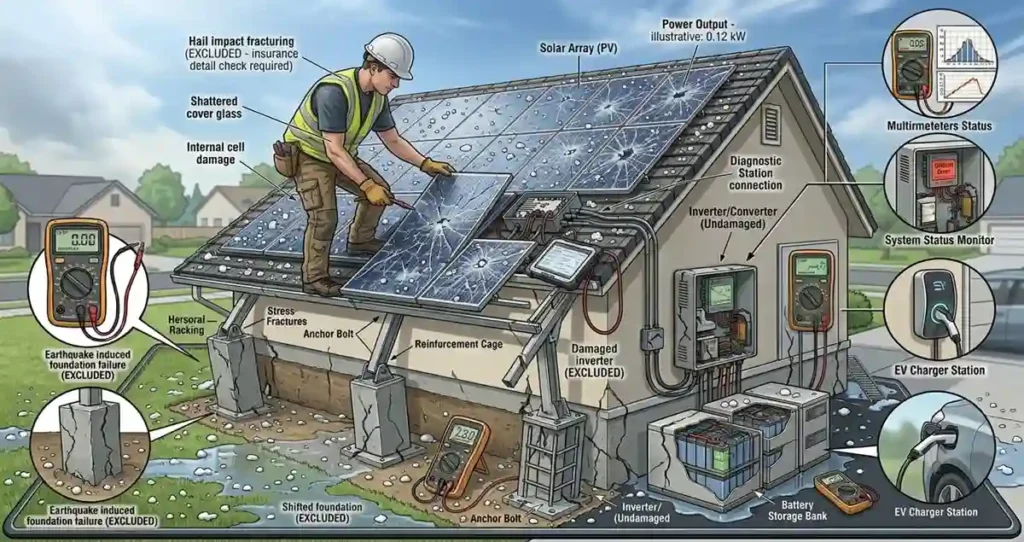

2. What Solar Panel Insurance Does NOT Cover — The Gaps

The standard HO-3 policy has exclusions that affect solar owners more than non-solar homeowners. Understanding these gaps before a loss event is what separates a covered claim from an out-of-pocket replacement.

| Common Exclusion | Impact on Solar Owners | Solution |

| Flood damage | Ground-mounted arrays in flood zones — not covered | NFIP flood policy or private flood endorsement |

| Earthquake damage | Racking failure, panel cracking from seismic event — not covered | Earthquake endorsement — critical in CA, PNW, and NV |

| Mechanical/electrical breakdown | Inverter failure due to internal fault — not a covered peril under HO-3 | Equipment breakdown endorsement (typically $25–$50/year) |

| Gradual deterioration | Panel degradation, cell delamination over time — not a covered loss | Manufacturer’s performance warranty — separate from insurance |

| Power surge (grid-side) | Grid surge damaging inverter or monitoring — often excluded | Equipment breakdown or utility service line endorsement |

| Cosmetic damage only | Hail dents with no functional impairment — insurer may deny | Document pre-loss condition; get manufacturer’s functional assessment |

| Field Note: The equipment breakdown exclusion catches homeowners off-guard more than any other. A string inverter that fails due to an internal capacitor fault after 7 years is not a windstorm or fire loss — it is a mechanical breakdown. The HO-3 does not cover it. An equipment breakdown endorsement covers exactly this scenario and typically costs less than $50 per year. I recommend it on every residential solar consultation. |

3. Which Solar Devices & Components Are Covered — Full Breakdown

Here is the component-by-component breakdown I walk clients through on every EPC project. The coverage category determines which dollar limit applies and whether a separate endorsement is needed.

| Device / Component | Avg Replacement Cost (US) | Standard Coverage | Endorsement Needed? |

| Monocrystalline solar panels (per panel) | $150–$400 | Coverage A — Dwelling | No — if within Coverage A limit |

| String inverter (5–10 kW) | $1,000–$2,500 | Coverage A — Dwelling | Equipment breakdown for internal fault |

| Microinverters (per unit) | $150–$300/unit | Coverage A — Dwelling | Equipment breakdown recommended |

| Solar battery (e.g. Tesla Powerwall 3) | $9,200–$11,500 installed | Coverage A if hardwired | Scheduled endorsement if value exceeds sub-limit |

| Racking system (per kW) | $200–$500/kW | Coverage A — Dwelling | No — structural component |

| DC wiring, conduit, combiners | $500–$2,000 full system | Coverage A — Dwelling | No |

| Solar monitoring system (e.g. Enphase) | $200–$600 | Coverage C — Personal Property | Scheduled endorsement if high value |

| EV solar charger (hardwired) | $800–$2,500 installed | Coverage A or B | Confirm attachment classification with insurer |

| Ground-mount racking & panels | Full system cost | Coverage B — Other Structures | Verify 10% Coverage B limit is sufficient for system value |

| Engineer’s Note: Battery storage is the component most likely to be underinsured. A Tesla Powerwall 3 costs approximately $9,200–$11,500 installed. If your insurer classifies the battery as Coverage C personal property with a $5,000 sub-limit, you have a significant gap. Get written clarification from your insurer on how they classify your battery system before purchasing. |

4. How to Check If Your Current Policy Covers Your Solar System

Most homeowners do not contact their insurer before installing solar. This is a mistake. Here is the exact sequence I advise EPC clients to follow:

| Step | Action | Why It Matters |

| 1 | Notify your insurer before or immediately after installation | Some policies require notification to maintain coverage; failure to notify can void a solar-related claim |

| 2 | Request written confirmation that panels are covered under Coverage A | Verbal confirmation is not binding — get it in writing |

| 3 | Confirm your Coverage A dwelling limit includes the full system value | A $25,000 solar system on a home insured for $300,000 raises replacement cost — verify your limit is updated |

| 4 | Ask specifically about inverter and battery coverage classification | These components have the highest mechanical failure risk and may fall outside standard HO-3 limits |

| 5 | Add equipment breakdown endorsement | Covers inverter and battery failures from internal faults — HO-3 does not |

| 6 | Confirm ground-mounted array falls under Coverage B and limit is sufficient | Coverage B is typically 10% of Coverage A — verify this covers your full system value |

| 7 | Review annually as system value and policy limits change | Panel replacement costs change; battery additions need to be added to the policy |

5. How Much Does Solar Panel Insurance Cost?

In most cases, adding solar panels to a home that already has homeowners insurance does not significantly increase the premium — because the panels are covered as part of the dwelling. What increases the premium is raising your Coverage A limit to reflect the added system value.

| Coverage Addition | Typical Annual Cost Increase | Notes |

| Dwelling limit increase to cover $20,000 system | $50–$150/year | Depends on insurer, state, and existing premium |

| Equipment breakdown endorsement | $25–$50/year | Covers inverter/battery mechanical breakdown |

| Scheduled battery endorsement | $30–$80/year | For battery systems exceeding standard sub-limits |

| Earthquake endorsement (CA/PNW) | $100–$400/year | Highly location-dependent — critical for seismic zones |

| Flood endorsement / NFIP | $700–$1,200/year | For ground-mounted arrays in flood zones |

| Field Note: The most cost-effective insurance move for a new solar owner is a $25–$50/year equipment breakdown endorsement. The most expensive mistake is not updating the Coverage A dwelling limit to reflect the full installed system value. If your system costs $28,000 to install and your insurer pays out at the pre-solar dwelling value, you are self-insuring a $28,000 asset. |

Frequently Asked Questions

Does homeowners insurance automatically cover solar panels?

In most cases, yes — rooftop solar panels are covered under Coverage A as a permanent dwelling fixture under a standard HO-3 policy. However, you must notify your insurer, confirm the coverage in writing, and update your Coverage A limit. See the full guide: Does Homeowners Insurance Cover Solar Panels?

Does home insurance cover solar batteries?

Hardwired battery systems are generally covered under Coverage A. However, many policies have equipment sub-limits lower than the full replacement cost of a battery system. A scheduled endorsement ensures full replacement value coverage.

Does solar increase my home insurance premium?

Not significantly in most cases — but your dwelling coverage limit should be increased to reflect the system value. Full breakdown: Do Solar Panels Increase Your Home Insurance Premium?

What if I have a ground-mounted solar system?

Ground-mounted systems fall under Coverage B (Other Structures), typically capped at 10% of Coverage A. If your system value exceeds that cap, a scheduled endorsement or inland marine policy is required. For commercial ground-mount systems, see: Commercial Solar Panel Insurance

Related Guides on SolarVisionAI

Does Homeowners Insurance Cover Solar Panels? Complete Guide

Do Solar Panels Increase Your Home Insurance Premium?

Commercial Solar Panel Insurance: Installers, Cleaners & Buildings

Solar Panel Hail Damage: What Your Insurance Covers